Getting Even

A Spotlight on...ransom notes, colonial repair shops, The Innovator's Dilemma, and an Indian startup fixing to remove luck from the business of staying alive

Hey folks👋

Long time no see! A happy (relatively) new year, and a warm welcome to the 2972 new Tigerfeathers subscribers who’ve joined since our year-end piece (the official one and the unofficial one).

We’ve got an epic line up in store for 2026, starting with today’s edition. So if someone sent you a link to this newsletter and this is the first time you’re discovering our stuff, subscribe below to make sure you don’t miss the next one.

Also, if someone sent you a link to this newsletter and you just noticed how long this piece is, we’d like to offer an apology on their behalf - it’s kind of the vibe here🤷♂️

Tigerfeathers is presented by…Dhan

India’s capital markets have spent the better part of a decade playing catch-up with the sophistication of the people using them. Most trading platforms either chased first-time speculators with gamified interfaces, or served institutional clients with tools inaccessible to the serious retail investor. Raise Financial Services was founded to fix that — and in the five years since, it has become one of India’s most celebrated fintech success stories: a profitable, product-first challenger that in October 2025 closed a $120M Series B led by Hornbill Capital, with participation from BEENEXT and Japan’s MUFG.

Their flagship product, Dhan, builds for experienced traders who need speed and precision, and thoughtful long-term investors focused on compounding wealth. That means advanced charting with TradingView integration, lightning-fast execution via a proprietary trading engine, and real-time portfolio analytics designed to help users make better decisions. Over 10 lakh traders and investors use the platform today.

Raise’s ambitions haven’t stopped at the trading terminal. Their ecosystem now spans Upsurge, a financial education platform; ScanX, a markets research and screener tool; and Filter Coffee, a bite-sized media product for the next generation of Indian investors.

The newest addition is Fuzz — an AI research assistant purpose-built for India’s financial landscape. Unlike generic AI tools trained to summarise, Fuzz is built to verify, backing every answer with traceable public sources. It runs on Artham, Raise’s own 7-billion parameter small language model trained exclusively on Indian capital markets data — the first of its kind, and notable enough to be spotlighted at AWS re:Invent 2025.

If you’re looking to level up your investing toolset, consider joining the Dhan community here, or check out the platform below:

And if you’re interested in sponsoring a future edition of Tigerfeathers, hit us up on Twitter/LinkedIn or by replying to this email. With that, let’s get to it.

If you’re in a hurry, and you’re looking for four generally applicable lessons to take away from today’s essay, they would be -

To shoot your shot.

To follow your curiosity, and follow it all the way.

To treat the Internet as a serendipity machine.

To design healthcare systems in a way that align the incentives of the entity delivering the care and the entity paying for it, so the most profitable outcome for the system is also the best outcome for the patient at the centre of it, and everyone makes more money by keeping you healthy than treating you when you’re sick.

Super generally applicable, just like we intended.

That being said, if tidy summaries aren’t your thing, and you’re down to follow us into the weeds, allow us a few paragraphs to give you the backstory on both the author and subject of this week’s Spotlight edition. Given that the actual essay veers dangerously close to book-length, you can treat this introduction as more of a prologue than a preamble (which means both are longer than you’d prefer them to be😬).

Anyway, strap in. We’ll kick things off in September 2025.

Rewind

On the 10th of September last year, The Ken announced the second iteration of its annual case study competition.

Describing the 2025 edition as more of a “case build” competition (*hipster attribute intensifies*) compared to the year prior, the company again invited college students from across the country to pick a real-world incumbent - any company, any sector, anywhere - and design a plan to disrupt it using AI. They upped the ante by challenging students to go beyond the slide deck to build working prototypes, landing pages and functional products to demo their solutions. The winning team could expect a cash prize of INR 10 lakh.

1,084 teams from 127 colleges across the country ultimately sent in a submission. After several rounds of evaluation, a hundred made it to the semifinals, with ten teams finally battling it out for the top prize at the last stage.

One amongst those hundred semi-finalist teams was a student from the Manipal Institute of Technology - Debarun Karmakar.

Into the Spotlight

Debarun was (and still is) in the third year of an undergraduate degree in Computer Science. Growing up in Pune, he spent a chunk of his childhood “in and out of hospitals” dealing with recurring health issues, embedding in him a fascination with the world of healthcare. It’s why, for his case study application, he chose to ‘disrupt’ Narayana Health (NH), India’s largest private hospital network.

NH was founded by legendary cardiac surgeon Dr. Devi Prasad Shetty, and has long been celebrated as the gold standard of low-cost, high-quality healthcare on the Subcontinent. Debarun’s decision to take on NH was emboldened by the fact that, anytime he needed inspiration, he could basically saunter out of his dorm room and stroll ten minutes down the road to the campus of Kasturba Medical College (KMC) and it’s equally vaunted chain of partner hospitals in Manipal.

For three months, Debarun did what any good disruptor is supposed to do - he searched for blindspots and vulnerabilities. He spent time at KMC, walking the wards, talking to doctors and administrators, even peppering the leadership of Manipal Hospitals with questions around their biggest headaches and dream solutions, slowly building a picture of how a major healthcare institution actually works from the inside. He got a privileged audience with Viren Shetty, Narayana Health’s CEO, who’d benevolently made himself available as a resource to all the case study teams that had (rudely) elected to take aim at his institution.

These conversations were illuminating. After passing by the kinds of pointed complaints that sit at the edges of Indian healthcare (lengthy receivables cycles, delays in discharges, limited personal attention from doctors at busy hospitals etc), he finally arrived at the fault line that runs through the entire system.

Case/Build

The big problem - the one that was upstream of so many other problems - was the structural tug-of-war between payer and provider: insurers, patients, doctors and hospitals who weren’t just separate parties, but whose financial survival depended, in ways large and small, on outcomes that were fundamentally at odds with each other.

What does that really mean?

As Debarun found, here’s a mundane example that plays out in hospitals across India every day: A patient comes in with a complaint. Tests are ordered, specialist doctors are consulted, an admission is recommended. Each of these decisions may be entirely legitimate, but each one also happens to generate revenue for the hospital and the doctor. The insurer, on the other side, is looking for any reason to limit the payout (finding the exclusion clause, the pre-existing condition, the technicality that limits the payout etc). So one half of the system is economically oriented to doing more, rather than better, while the other half is looking for ways to pay less. Nobody in this transaction is behaving illegally or even unethically. Hospitals aren’t villains, doctors aren’t charlatans, and insurers aren’t cartoon antagonists. They’re just each defaulting to the incentives imposed by the structural reality they operate within. The trouble is that those incentives don’t always align with yours.

By the way, this isn’t just a mundane example, it’s an entirely ubiquitous dynamic found not only in India but in virtually every for-profit healthcare market in the world. It’s a tension that serious money has been working to resolve for decades. In the US, Kaiser Permanente has operated a fully integrated payer-provider model since the 1940s - and with 13 million members, 55 hospitals, and $115 billion in annual revenue, it remains the most compelling proof that the model really works. It’s why companies like CVS Health, America’s largest pharmacy chain, spent $69 billion acquiring Aetna, one of the country’s biggest insurers, in 2018. Closer to home, Narayana Health itself had arrived at the same conclusion — launching its own standalone insurance product, Narayana One Health, in mid-2024, becoming India’s first hospital-owned insurance brand. The execution has proven harder than expected.

For a potential disruptor looking at this situation from the outside in, the flaw is obvious - and so is the opportunity. If the root problem is that payers and providers are separate entities with misaligned incentives, the solution writes itself: smush them together in the same entity.

What you’d get is one company that insures you, employs your doctors, runs your diagnostics, and maybe even owns your hospital - so that the most profitable thing it can do is also the best possible thing for you i.e. keep you healthy, keep you out of hospital, and never give you a reason to make a claim. Any amount spent on your health and wellness is a cost that pays for itself - a teleconsult today is cheaper than a hospitalisation next year, a preventive screening now is cheaper than a chronic disease later, and a fitness tracker is considerably cheaper than a cardiac surgery. In practice, it could look something like a ‘Spotify for healthcare’ - a single monthly subscription that gives you unlimited access to consultations, check-ups, and diagnostics, underwritten by an entity that makes more money the healthier you stay.

On paper, it is an elegant solution. It’s also a solution that formed the heart of Debarun’s case study submission to The Ken - his theoretical disruptor to Narayana Health - something that looked like a ‘Kaiser Permanente for India’. He didn’t make it past the semifinals, but he left convinced there was something concrete here, something worth building on.

The good news was that he had discovered a genuine opportunity - a real problem in a massive industry (two massive industries), that an entity with no incumbent baggage could conceivably exploit. Unlike the US, no legacy institution had cracked this model at scale in India, and the door was wide open for exactly the kind of new entrant Debarun was imagining. The bad news, as he soon discovered, was that someone else had already walked through it.

Breaking Even

‘Two Italians and an Indian with no medical expertise walk into a hospital…’ is probably a serviceable premise for a joke somewhere in the world. In the case of Even, it has proven a surprisingly excellent premise for a healthcare startup in India.

Even Healthcare was founded in 2020 by the trio of Mayank Banerjee, his friend and former co-founder (at news media startup Compass News) Matilde Giglio, and her childhood best friend and machine learning engineer Alessandro Ialongo.

The apparent disconnect between their backgrounds and their choice of business makes more sense when you consider that the ideological foundation of Even isn’t rooted in healthcare at all - it’s rooted in fairness.

For Mayank, a personal tragedy in his teenage years had made him viscerally aware of how the outcome of a medical emergency in India often hinged more on who you knew and how much money was in your pocket, rather than the quality of care you received and how badly you needed it. Healthcare was an apparent luxury for so many on the Subcontinent, with 5.5 crore (55 million) Indians being thrust into medical bankruptcy every year because of a single hospital bill. So despite spending his formative years in the UK, he moved back to India, to Bangalore, on New Year’s Eve in 2018, determined that India - with its scale, its urgency, and the sheer number of people on the wrong side of fairness, presented a more dire set of problems-worth-solving than anywhere else in the world.

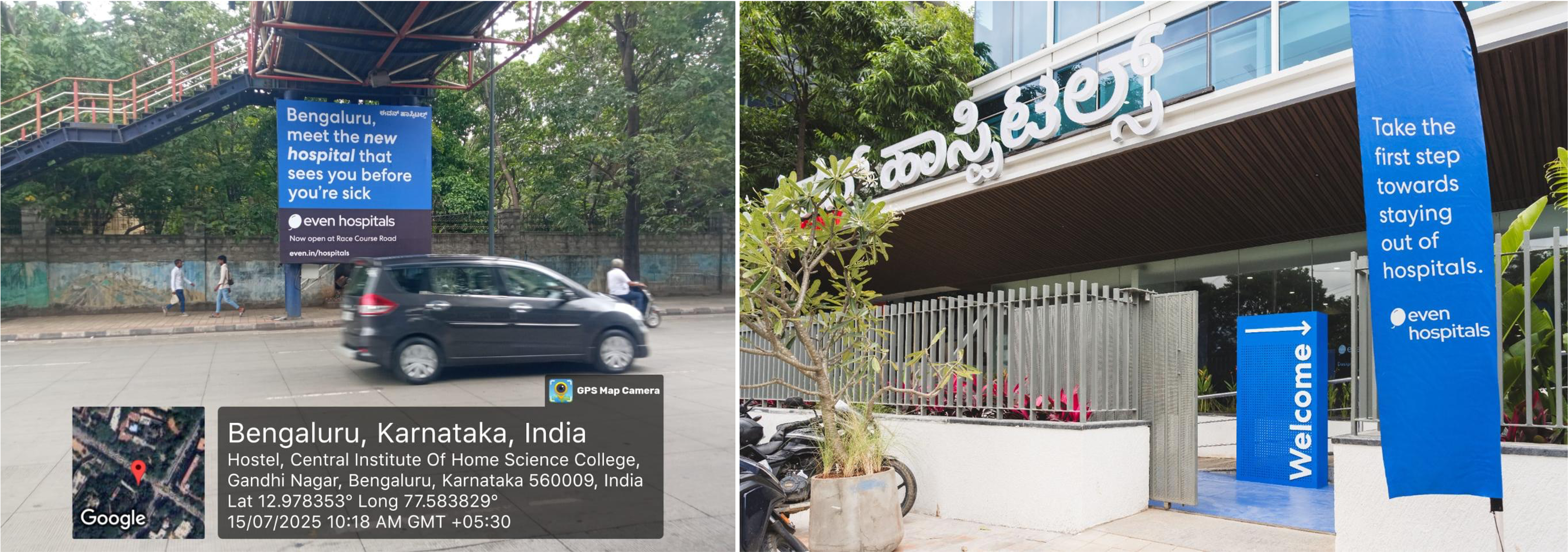

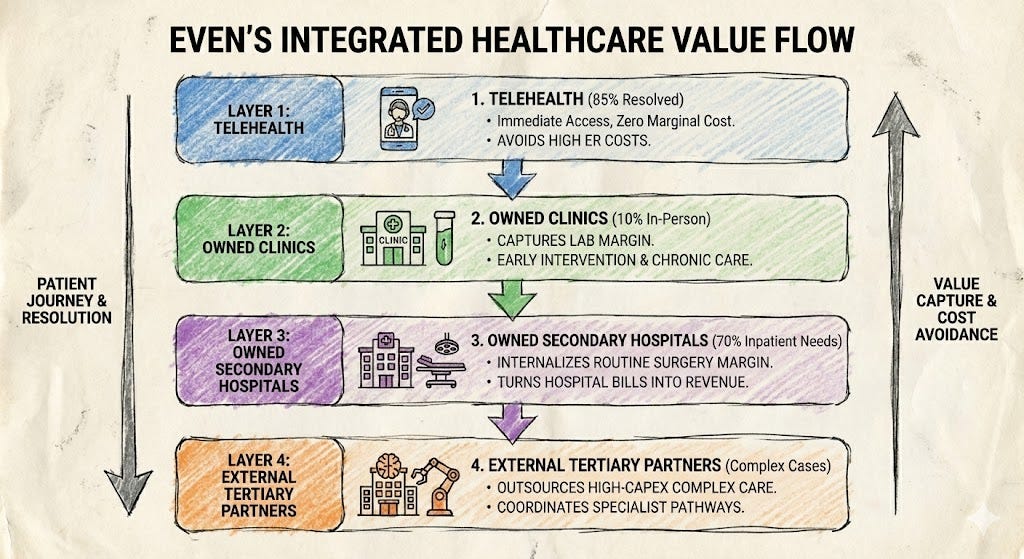

Eventually joined by Matilde and Alessandro in 2020, Even began its operations by offering customers a hospital membership plan - pay a fixed monthly fee, and your hospital bills are covered across their partner network. Today, after five years in the idea maze, their offering has morphed into something closer to a universal healthcare subscription - a single plan that covers unlimited doctor consultations, unlimited diagnostics, and a hospitalisation cover powered by their insurance partners in the background. To fully deliver on their promise and align the focus of every participant in their value chain, Even employs its own team of doctors and specialists across its own network of clinics and diagnostic centres — culminating in mid-2025 with the opening of its first hospital on Race Course Road in central Bangalore, built from scratch in seven months, with several more already in the pipeline.

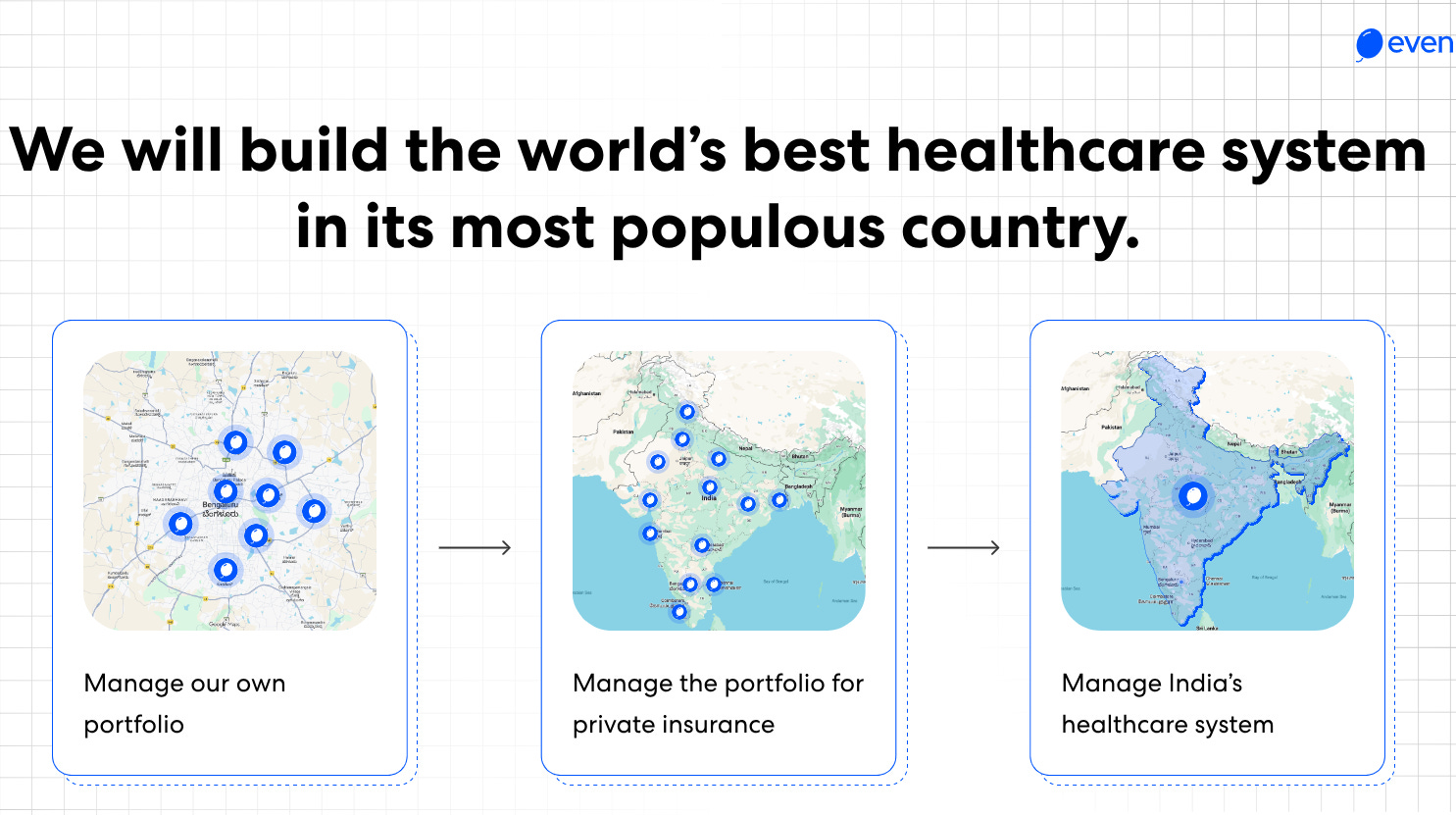

To us, Even is an Indian startup (and story) that merits close examination, because if all rolls their way, what they hope to have produced over the next 5-10-15 years, is not just a single successful company. What they hope to prove is the viability of a new model for healthcare in India, one that is more equitable, profitable, and replicable than anything that exists right now. Those are the stakes.

But despite all this activity and ambition, Even is in the curious position of being perhaps more well known in San Francisco than it is in India. That’s partly because its work so far has been concentrated within Bangalore, and partly because it sits in the portfolios of several of Silicon Valley’s investing heavyweights. As of the closing of its most recent $20 million round in January 2026 (bringing its total funding to $70 million), Even counts on its cap table Vinod Khosla’s Khosla Ventures, Joe Lonsdale’s 8VC, and Physical Intelligence’s Lachy Groom, among other Indian and American tech luminaries, and carries the distinction of being the only Indian company currently in the portfolio of Peter Thiel’s Founders Fund.

It would be fair to say, though, that it’s not a household name in India yet. Which makes it, for now, a company that’s flown a little bit under the radar of the wider tech ecosystem. It means its disruptive business model has yet to be appreciated outside the healthcare ecosystem, even if you were the kind of person specifically looking for ways to disrupt the Indian healthcare industry…

How We Got Here

“All the ideas I had for new healthcare business models, it felt like Even was already implementing all of them,” says Debarun. “They were somehow reducing costs, improving outcomes, and reducing readmissions, and making it make business sense for themselves and their partners.”

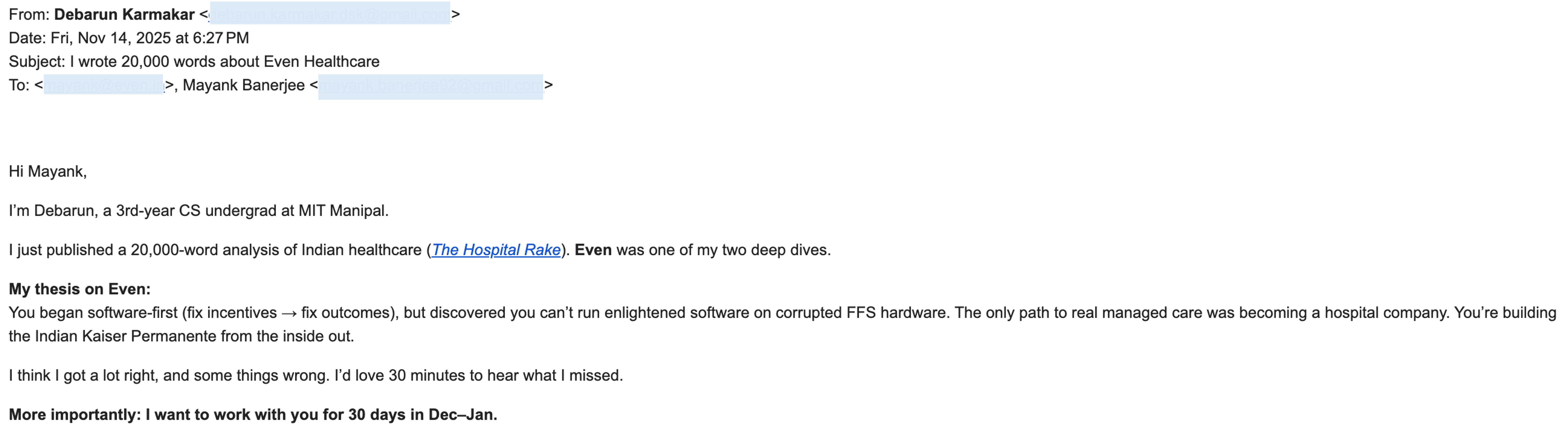

As he dove further into his research on payer-provider business models after bowing out of the case study competition, Debarun finally discovered the work being done by Even and other pioneering Indian healthcare startups, like Varun Dubey’s Superhealth. He turned all of this research, including his primary findings on the problems ailing Indian hospitals and insurers, into a biting 20,000-word Substack post titled ‘The Hospital Rake’. He then put this essay to work, using it as the centrepiece of a cold email to Even’s Mayank Banerjee.

It worked.

Mayank was blown away by the piece, and immediately shared it with his co-founders. “He understood the different pieces of our operation and how they all fit together,” he recalls. “It’s something that usually takes multiple hours and conversations with investors. He knew what we were trying to accomplish in the short term, and correctly surmised what our long term plan was. It was the best thing anyone had ever written about us.”

The Even team invited Debarun to join them as part of the Founder’s Office for the duration of his December break from college. He packed his bags and moved to Bangalore shortly thereafter.

Coincidentally around the same time, we started chatting with Mayank about doing a Tigerfeathers piece on Even in early 2026. During those conversations, Mayank told us about ‘this college kid who’s written this awesome piece on Even that’s worth checking out’. We did. We were impressed.

The writing was sharp, the thinking was clear, the ideas were fresh and opinionated, and the author didn’t have to use any juvenile memes to get his point across.

Outside of any of that stuff, it was just fun to read, and you could tell the author enjoyed creating it too. Around 500 words in, it became clear that 1. there was no way we were writing a better piece on Even or on healthcare in India; 2. this was clearly an exceptional writer writing about a subject he was super passionate about.

You also have to be a little dumb to expect people to read a 20K-word blogpost in 2026, so it came as no surprise to us that he was a longtime Tigerfeathers subscriber (the only thing that worked against him). We reached out to him in December and asked if he would do a v2 of his original essay as a Spotlight piece once his stint with Even ended, presumably informed and sharpened by his time inside the company and his subsequently acquired first-hand knowledge of Indian healthcare, with an expanded scope that included:

Researching the colonial origins of the Indian healthcare system, and explaining why it was never actually designed to cater to the people it currently serves

Unpacking the structural economics of hospitals and insurers, and the perverse incentives that make everyone in the chain behave rationally while the patient pays the price

A rigorous autopsy of why every attempt to fix the value chain has fallen short in the same predictable ways, and how the system often fails the most vulnerable of Indian patients

Why the Even story is different and important - the origin, the model, the near-death experience, and what it means to build a hospital

Why the incumbents can see exactly what Even is doing but can’t just copy it, and what all of this means for the future of healthcare in India

That’s what today’s piece is.

It has taken almost three months, several edits, and an insane amount of work to get here. What Debarun’s produced is a 28,000-word monument to the past, present and future of Indian healthcare - to what is broken, what is promising, and what is at stake.

It is a testament to what happens when someone honours their curiosity by following the thread all the way to the end. It’s the kind of piece that will make you look at the world a little differently, or at least at a tiny part of it. We are all the more grateful for the effort he’s put in given the start of his mid-term exams this past Monday (if any of his teachers are reading this, pls dear sir/madam give this man THE BEST GRADES ONLY - he deserves it).

Anyway, we hope you enjoy reading it as much as we did. This is almost certainly not the last time you hear from Debarun this year. We’ve basically brought him into the Tigerfeathers fold to contribute to what we’re doing on the media and investing front this year (at least until he gets bored or too busy with college work). Watch this space for more from him👀.

With that said, lets get on with it.

Hey Tigerfeathers readers, Debarun here. Here’s a quick note on methodology before we get started: This piece draws on financial filings from publicly traded hospital chains and insurers (Max, Fortis, Apollo, Star Health), Even Healthcare company interviews and operational data, published research on integrated care models (Kaiser, Optum, Hapvida), IRDAI regulatory data, and WHO/National Health Accounts data on Indian healthcare spending. We’ve toured Even’s hospital, interviewed leadership, and reviewed internal financial models. Some specific numbers are approximated or withheld to protect company confidentiality. Where this creates uncertainty, we’ve noted it explicitly.

[I] What Does the Perfect Business Look Like?

There’s a business model that gets pitched in private equity meetings that sounds, on paper, like the most beautiful thing in the world. The cash flows arrive like clockwork, the customers have zero bargaining power, the physical infrastructure creates a moat, and the total addressable market is…literally everyone.

To top if all off, the return on capital employed is magnificent, and the EBITDA margins are north of 25%.

We are talking about a veritable multi-decade compounding machine. Also known as a hospital.

Let’s diagram a simple, commonplace transaction in the Indian healthcare market. You have two parties: a Creditor and a Debtor.

The itemised bill reads:

Cardiac catheterisation and stent: ₹2,20,000

Two nights in ICU: ₹1,50,000

Diagnostic imaging (ECG, stress test, angiogram): ₹95,000

Medications and pharmacy: ₹45,000

Doctor consultations and fees: ₹34,000

The number on the paper sums up to ₹5,44,000. Roughly $6,000.

It’s a large part of your annual income, which is inconvenient, because you hadn’t planned a major medical event between rent and groceries.

Your mother came in with chest pain. The doctors ran tests. Good tests. Thorough tests. An ECG, a stress test, a full cardiac panel, imaging. The cardiologist expressed “clinical concern,” which is a professional term that often precedes doing a lot more things that involve expensive machines. They did an angiogram, found a blockage, and put in a stent.

Two nights in the ICU, some pills, and a few follow-up appointments later, your mother is stable. The care was excellent. The facility was clean. Everything worked exactly as it should.

Except the bill.

You ask the only question available: “Is all of this necessary?”

The billing administrator looks at you with practiced sympathy. She didn’t make up the price. She’s showing you line items that all have medical codes, approved procedures, standard rates. The doctor followed protocols, ordered appropriate tests, and made clinically sound decisions. The hospital didn’t build expensive cardiac catheterisation labs for fun. These machines cost crores, and once they exist, they need to be used to justify their existence and pay back the debt that financed them.

Everyone is more or less doing their job.

This is not a story about bad people and evil math. This is a story about good people and unfortunate math.

Hospitals cost a lot to build and run, and once they exist, the sensible financial move is to use them as much as possible. When the hospital runs more tests, does more procedures, keeps you for extra observation days, i.e. when more billable things happen to you, more capital gets repaid. The MRI machine’s loan gets paid down a little faster. The catheterisation lab justifies its existence. The building moves closer to profitability. It’s just how the system is wired.

None of this is visible to you, standing in the corridor outside your mother’s room, holding a piece of paper with ₹5,44,000 printed at the bottom. You’re not thinking about debt service schedules or utilisation rates. You’re thinking about how a number this large appeared at the end of what felt like completely normal medical care, and whether any of it was actually necessary, and whether “necessary” is even a question you’re allowed to ask at this point.

But wait…what’s that in your back pocket? It’s…Insurance. You have insurance. Thank god. You’ve been paying ₹18,000 annually for the last three years for exactly this situation.

The insurance company reviews the file. Several procedures are being questioned.

“Medical necessity not established for pre-procedure imaging.”

“Observation period exceeds standard protocol for this intervention.”

“Pharmacy charges include non-formulary medications.”

“Claim partially denied. Approved amount: ₹2,69,000.”

Your responsibility: ₹2,75,000.

You call the insurance company. The representative is polite but firm. The policy has terms, you see. The hospital billed above standard rates. Some procedures weren’t pre-authorised. But don’t worry, there’s an appeals process if you disagree.

You call the hospital. They explain they can’t negotiate the bill downward, policy determines rates, and you received the care. If you had concerns about costs, you should have discussed it before the procedures.

Neither party is lying. Both are following their rules. The outcome is that you’re out ₹2,75,000 for your mother’s heart problem, and you’re not even sure which parts were “necessary” and which parts were “hospital needs to justify expensive equipment.”

Now comes the part nobody tells you about in the glossy hospital brochures.

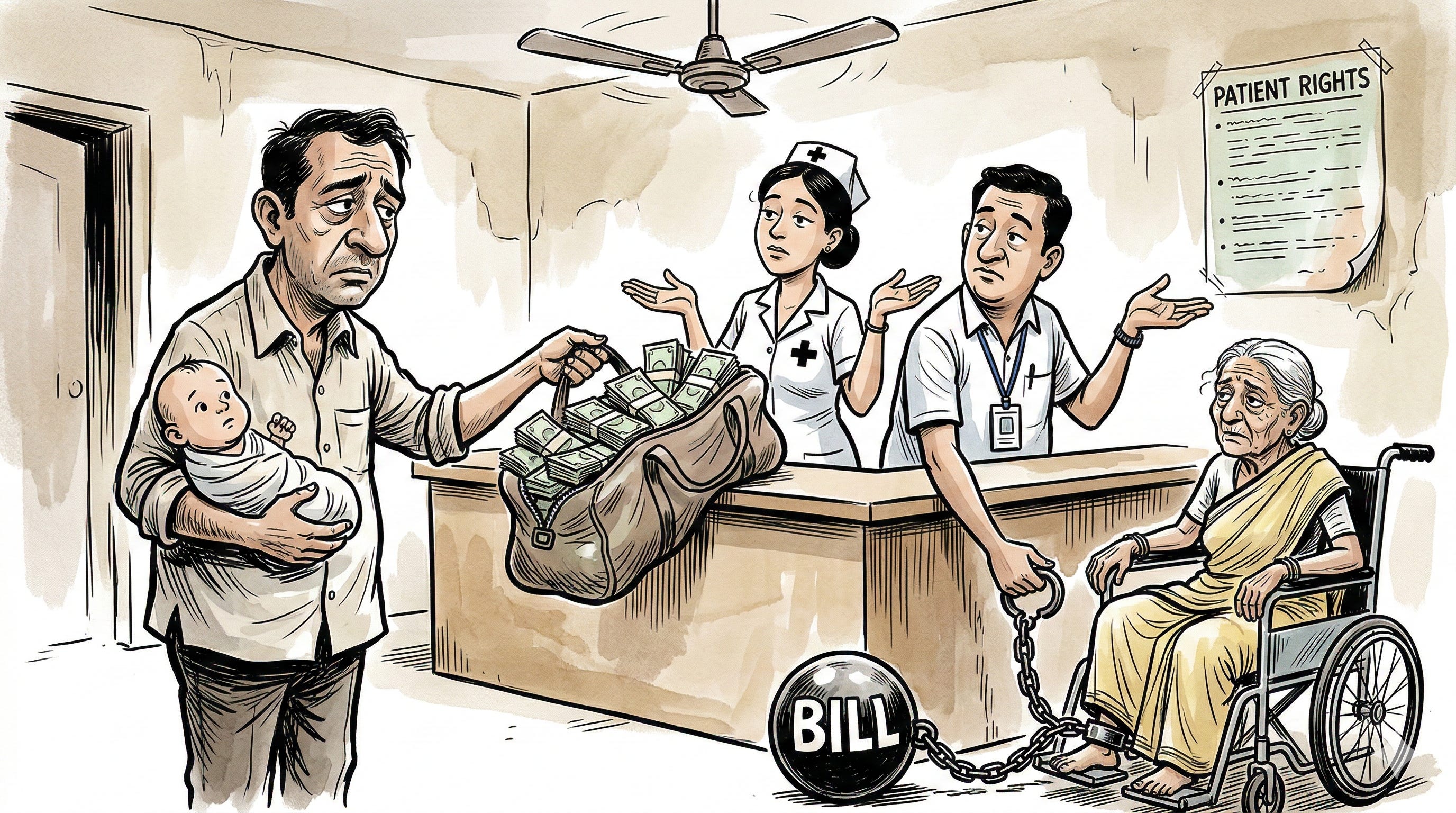

₹2,75,000 is not a number that exists in your bank account. Your household brings in ₹8 lakhs a year. You have maybe ₹40,000 in savings. The hospital knows this, has always known this, because the ‘Estimate Desk’ (more on this later) clocked you the moment you walked in without a car, reading the specific kind of anxiety that signals limited liquidity.

Your mother is medically cleared to leave. But the discharge paperwork sits unsigned on the administrator’s desk. The insurance has paid its portion. The remaining ₹2,75,000 must be settled before she goes anywhere. This is not a negotiation. It is a countdown. Seventy-two hours.

What happens next is a forced liquidation event that plays out in millions of Indian households every year:

Your father makes calls to family members. An uncle in Mysore has a Provident Fund he can borrow against, but the paperwork will take four days and there’s a 10% penalty. Your brother-in-law has a mutual fund investment, ₹1.2 lakhs, but redeeming it now means a 15% short-term capital gains hit. Your mother’s brother offers to sell some agricultural land, the family’s only appreciating asset, but in a fire-sale it will fetch maybe 60% of its actual value.

You pool these emergency liquidity sources like you’re assembling a ransom payment. Because functionally, that’s exactly what this is. The hospital has something you need - your mother’s discharge and dignity and the price is non-negotiable.

Three days later, you return to the billing office with a bag containing:

₹80,000 in cash withdrawn from your father’s PF (with penalties)

₹1,00,000 from your brother-in-law’s liquidated mutual fund

₹95,000 from the distress sale of farmland that’s been in your family for two generations

The hospital administrator counts it, generates a receipt, and hands you the discharge summary. Your mother can leave now.

This transaction, from the hospital’s perspective, is a masterclass in operational excellence. Zero receivables. No payment plans. No defaults. Cash on the barrel, collected at the point of maximum leverage. The hospital’s balance sheet records this as “revenue,” and the family’s balance sheet records this as “catastrophic health expenditure,” but these are just two ways of describing the same transfer of wealth.

The medical emergency is over. The financial emergency has just begun. The mutual fund that was meant to fund your brother’s wedding is gone. The farmland that was supposed to be your parents’ retirement security is gone. The Provident Fund that was your father’s hedge against unemployment is depleted.

You did what you had to do. And so did fifty-five million other Indian families this year.

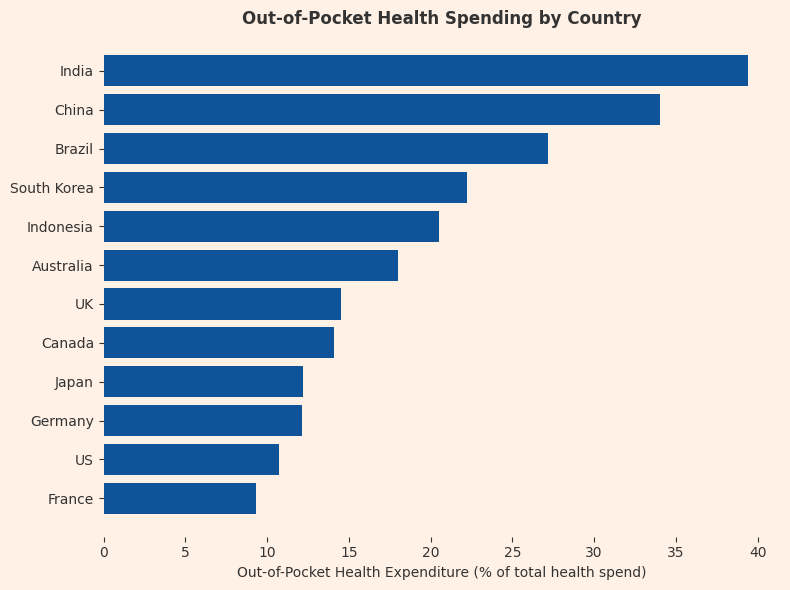

Now scale this single transaction from above across a country of 1.4 billion people and the macro picture starts to look a bit extreme.

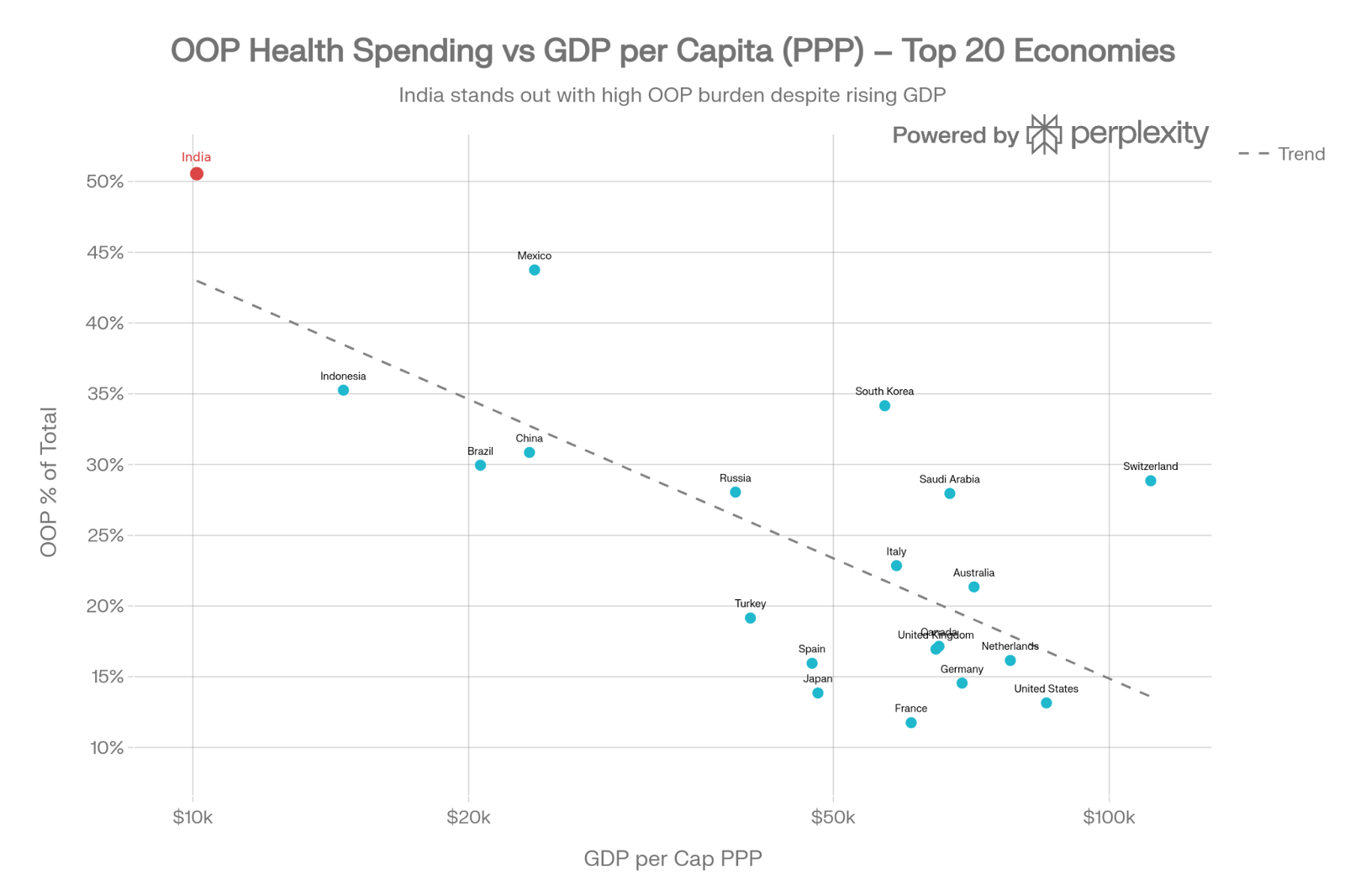

India funds roughly 39.4% of its healthcare the old-fashioned way, by reaching directly into wallets at the worst possible moment. Every year, more than 55 million Indians face medical bankruptcy. That’s the entire population of Canada being pushed below the poverty line annually because someone got sick.

And here’s the part that should make you close your laptop and stare into the void: all of this means private hospitals are excellent businesses.

The distinction matters. Public hospitals in India operate under an entirely different logic - chronically underfunded relative to need, they nonetheless serve the majority of India’s population and remain the primary option for hundreds of millions who have no private alternative.

The private hospital sector, which now accounts for roughly 70% of all healthcare delivery in India, operates under an entirely different logic.

Demand is steady and rising. Supply is structurally constrained. Prices are opaque. The customer rarely chooses based on cost. Payment is increasingly routed through insurers and governments, which dulls price sensitivity further, but when it fails, the collection mechanism we just witnessed kicks in with brutal, mechanical precision. In almost any other industry, this would be described as pricing power.

And hospitals sit at the centre of that dynamic. They control the physical assets (the beds, the machines, the expertise). They control the moment of maximum leverage (the emergency, the discharge, the “estimate desk”). They control the information (what’s necessary, what’s standard, what’s negotiable). They are simultaneously the service provider and the debt collector, the caregiver and the creditor.

The system isn’t failing. It’s doing exactly what it was designed to do - optimise throughput, billing, and utilisation. Health just isn’t one of the variables it’s rewarded for improving.

You can’t fix this by asking hospitals to act against their own economics. You have to change who holds the risk, who controls the assets, and when money is made. You have to redesign the system so that the most profitable thing to do is also the healthiest thing for the patient.

But to understand why that’s so difficult, you need to understand how we got here.

[II] The Original Sin

The Accidental Enterprise

If you want to understand why Indian healthcare works the way it does, you have to realise that it isn’t really one system. It’s a series of historical accidents that someone eventually tried to turn into a business.

To understand this dysfunction, we have to go back to the era when healthcare was an HR function of the British Raj. The colonial government did not build healthcare in India to “help people”, rather it was designed to keep the colonial administration from dying. If you are running an empire, you need a repair shop for your administrators and your military. So, you build hospitals in the places where your employees happen to live - and in the mid-nineteenth century, that meant the three great presidencies: Bombay, Calcutta, and Madras.

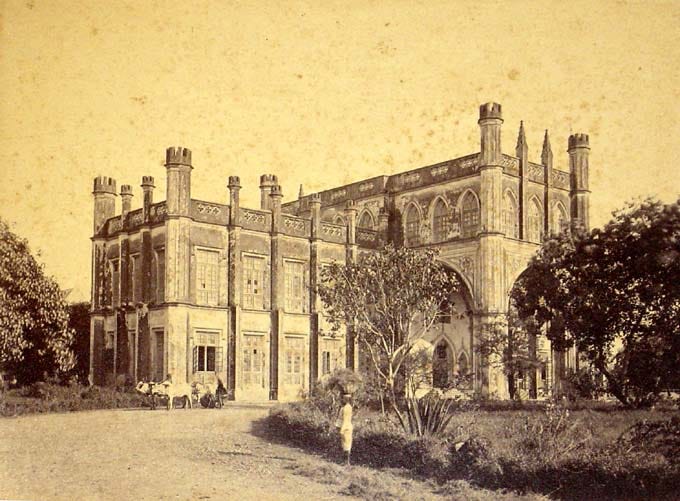

Let’s take Calcutta. The Medical College of Bengal, established in 1835, was the the first institution in Asia to teach modern Western medicine. But although it was built in the empire’s most important city it was not built to serve the city’s millions. Instead, its purpose was to ensure a British officer didn’t die of infectious disease before his pension vested.

Over on the west coast, Bombay got the Grant Medical College. Founded in 1845, it was a grand institution with marble floors, European-trained surgeons, and imported equipment. The standard of care matched what you would find in London. But the logic underpinning it was the same: keep the rulers functional, ignore everyone else.

After independence, India inherited this template. It was not dissimilar to inheriting a corporate campus designed by a company that went bankrupt in 1947: the plumbing is weird, the buildings are in the wrong places, and it was never actually intended for the people who live there now. The hospitals existed, but they were positioned for the needs of a departed empire, not a newly independent nation of 300 million people spread largely across disconnected villages and towns.

The Promise Of The Committee

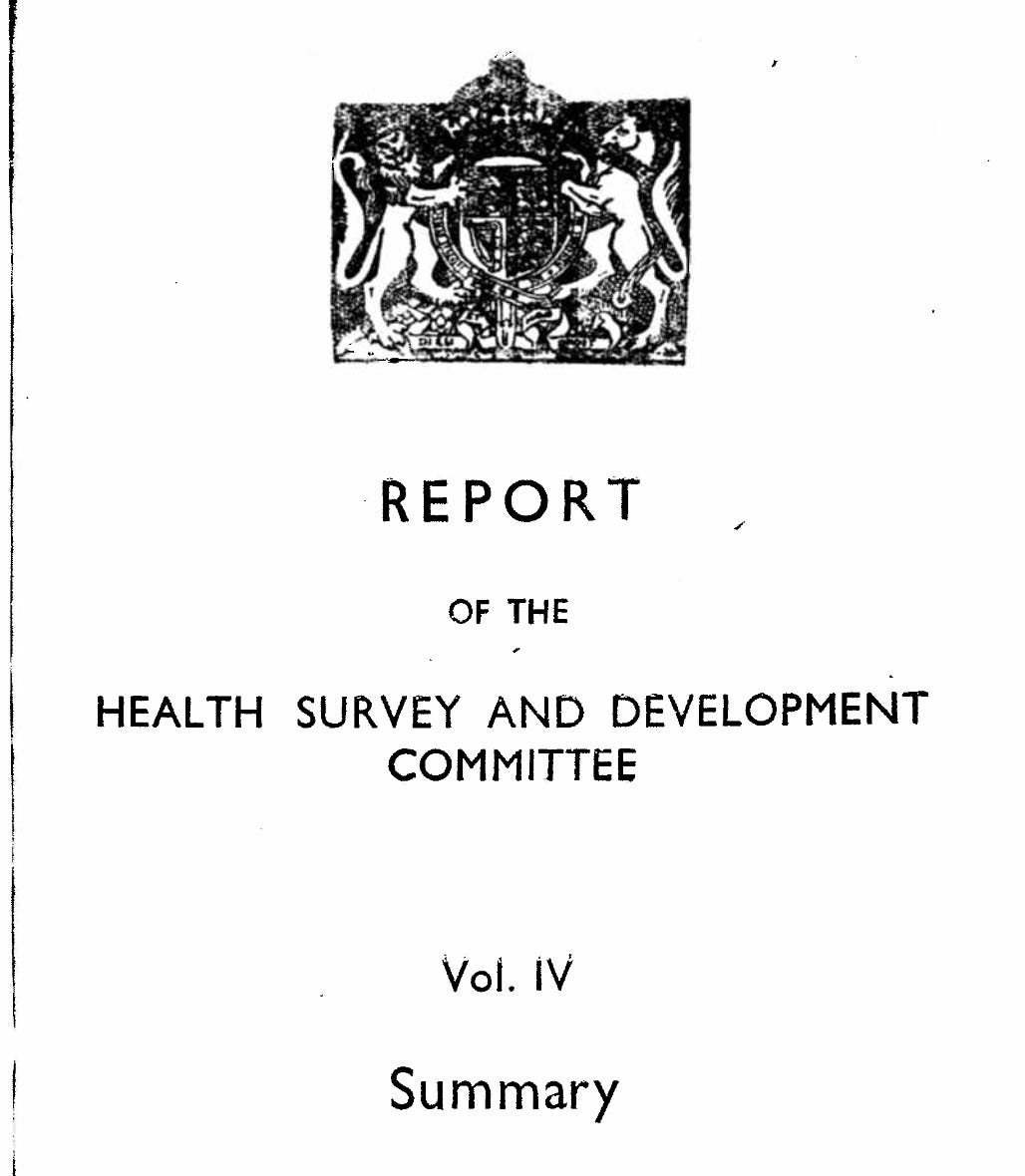

In 1946, the Bhore Committee, led by Sir Joseph Bhore and tasked with planning India’s health infrastructure from first principles, spent two years studying the country’s health needs and produced a vision so comprehensive it filled four volumes.

The report was extraordinary in its ambition and clarity. It envisioned a complete transformation: a national program of health services that would reach every village, integrate preventive and curative care, and train a new generation of “social physicians” who understood that health went beyond just treating disease and extended to sanitation, nutrition, and prevention.

The committee’s most striking passage captured both the scale of the problem and the urgency of the solution:

“If it was possible to evaluate the loss, which this country annually suffers through the avoidable waste of valuable human material and the lowering of human efficiency through malnutrition and preventable morbidity, we feel that the result would be so startling that the whole country would be aroused and would not rest until a radical change had been brought about.”

They weren’t wrong about the loss. What they underestimated was how difficult it would be to arouse the country, or more precisely, to arouse the country’s budget allocation.

The Bhore Committee proposed a two-stage rollout. Over the short term, one Primary Health Centre for every 40,000 people, staffed by two doctors, one nurse, four public health nurses, four midwives, two sanitary inspectors, one pharmacist, and supporting staff, was recommended for immediate implementation. These PHCs would handle basic care and refer complex cases upward.

The eventual plan was more ambitious: a comprehensive three-tier system with a 75-bed primary unit for every 10,000-20,000 people, feeding into 650-bed secondary hospitals at the district level, which would connect to 2,500-bed tertiary hospitals for the most complex cases. The entire country would be covered by an integrated grid of healthcare facilities, each level supporting the one below it.

But buried in those four volumes, easy to miss between the staffing ratios and bed counts, was a single line that cut to the heart of the matter: “Integration of preventive and curative services at all administrative levels.”

Read that again.

In 1946, a committee of bureaucrats and physicians looked at India’s healthcare problem and concluded that the only real solution was to stop treating prevention and treatment as separate activities, that the doctor who kept you healthy and the doctor who fixed you when you weren’t should be part of the same system, with aligned incentives and shared information.

They saw it clearly. They wrote it down. They put it in an official government report.

The report was a masterpiece of central planning. On paper, it was exactly what India needed: a rational, hierarchical system that could deliver care at scale while managing costs through appropriate triage and referral.

The government drew up maps and began implementation. By 1952, India established its first Primary Health Centre. By 1961, there were 2,800 PHCs dotting the country. By 1981, that number had grown to 5,300. On a map, it looked like the Bhore Committee’s vision coming to life, neat dots representing clinics scattered across the country, a grid of care covering the subcontinent.

The middle tier - district hospitals meant to bridge the gap between primary care and specialist treatment - got built too, after a fashion. Most major districts eventually had a government hospital. The buildings existed. The beds existed. But chronic underfunding meant they operated as overwhelmed referral dumps rather than the coordinated secondary care facilities Bhore had envisioned. A district hospital in rural Uttar Pradesh in 1975 was less a functioning healthcare institution than a place where PHC failures went to be confirmed.

The top of the pyramid told a different story. The All-India Institute of Medical Sciences, established in New Delhi in 1956, was genuinely world-class - a tertiary care institution that could hold its own against the best hospitals anywhere. AIIMS became a symbol of what Indian healthcare could be when properly funded and properly run. The government went on to build six more AIIMS campuses over the following decades (until 2014, after which the government built or sanctioned 20 more). They remained islands of excellence - exactly the colonial paradigm the Bhore Committee had set out to dismantle, now reproduced in independent India’s own image.

So why didn’t we scale to create an archipelago of islands? One constraint stood in the way: the budget.

The 1% Solution

Post-independence, the new government made healthcare a cornerstone of its socialist promise. The commitment wasn’t accidental - Article 47 of the Indian Constitution, adopted in 1950, explicitly directed the state to raise the level of nutrition and standard of living of its people and improve public health. It was a founding obligation, written into the document that defined what independent India was supposed to be.

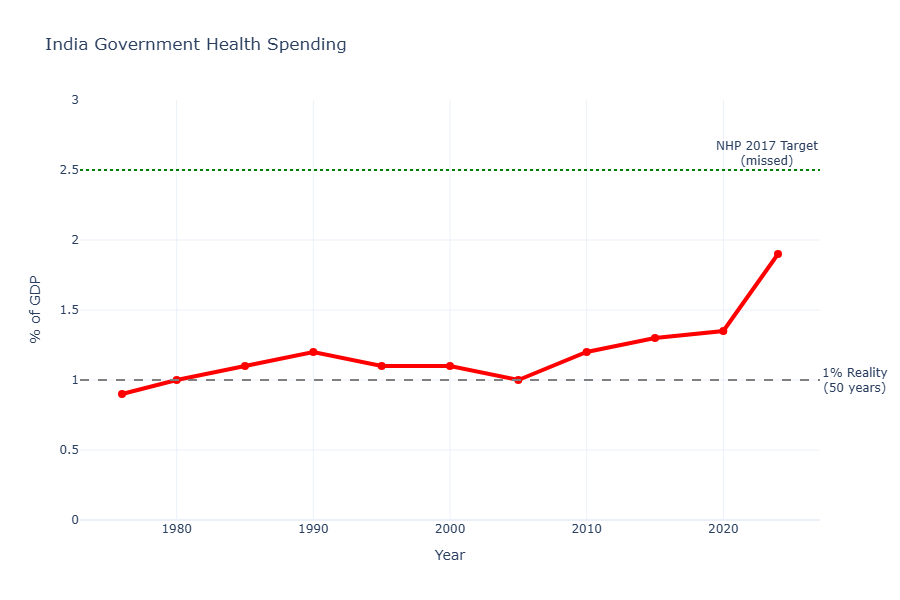

Here’s the problem with promising healthcare as a constitutional directive: directives require funding, and funding requires political will that survives contact with competing priorities. India’s government health spending has hovered around 1% of GDP for decades. For context, that is about what you’d spend if your plan was “hope nobody gets sick.” Middle-income nations usually spend 4-6%. Even other developing countries in the 1970s and 80s were spending 2-3%.

If you promise “Right to Health” but only fund 20% of what’s actually needed, you haven’t created a right. You’ve created a very expensive system to let people down.

On January 26, 1951, India’s second Republic Day, Rajkumari Amrit Kaur, the nation’s first Health Minister, published an essay describing what was already becoming clear.

Just three years after independence, she wrote:

“It is a real tragedy for India that very little attention has been paid to the nation’s health in the past... Independent India has had, therefore, to face a tremendous problem... We have got practical projects which we would like to undertake but we are handicapped by financial stringency.”

She catalogued what states were attempting: West Bengal launching hospital schemes on Bhore Committee lines, Uttar Pradesh opening rural dispensaries, Bihar experimenting with preventive health units. She described the tuberculosis crisis - 2 million sufferers, only 6,000 beds in 1947, doubled to 12,000 by 1951. Still serving less than 1% of those who needed them.

She acknowledged that “only a very small fraction of the revenues of the Government have in the past been devoted to Health.”

Then she ended with optimism: “The Ministry is confident that with the co-operation of the public and the medical profession, India will achieve a standard of health which will be the envy of other nations.”

She was describing, in real-time, the moment when the Bhore Committee’s comprehensive vision collided with “financial stringency.” The gap between “projects which we would like to undertake” and actual implementation would only widen over the next three decades.

The PHCs were built, or at least, buildings with “PHC” painted on them appeared in villages. But the buildings were shells. The doctors were missing, either never hired or hired and immediately transferred to cities where life was easier and corruption more lucrative. The medicine was perpetually out of stock because the procurement system was designed for bureaucratic compliance, not actual supply chain management. The equipment was broken, and stayed broken, because there was no maintenance budget and no one wanted to take responsibility for fixing anything.

?")

In the 1980s government studies found that 30% of PHC positions were vacant. In some states, the number was closer to 50%. The doctors who did show up often ran private practices on the side, treating government service as a part-time obligation. The “compulsory rural posting” required of new medical graduates became an elaborate game of connections and bribes to secure transfers to urban areas.

By the 1970s, a typical PHC looked like this: a concrete building, often well-constructed, sitting empty or staffed by a single underpaid nurse who showed up twice a week. The “doctor” listed on the books lived in the district capital and hadn’t visited in months. The medicine cabinet contained expired paracetamol and some dusty bandages. If you showed up with a serious illness, you were told to go to the district hospital 40 kilometres away, which had its own problems - no beds, no specialists, equipment that hadn’t worked since installation.

The rural poor, the people this system was ostensibly built for, quickly learned that the PHC was a place you visited if you wanted your time wasted. For anything serious, you borrowed money and went to a private doctor or traveled to a city hospital.

The gap between promise and reality became so vast it was almost comic. Government reports would dutifully count the number of PHCs established, the number of beds added, the quantity of medicine procured. None of these numbers bore any relationship to whether an actual sick person could actually receive actual care.

The system excelled at producing statistics. It failed at producing health.

The Great Exodus

By the 1980s, India’s public health system had become something paradoxical: it wasn’t a healthcare delivery mechanism as much as it was a “credentialing infrastructure” for doctors.

Medical colleges, many of them government-run, produced tens of thousands of doctors annually. These doctors were required to do a rural posting, a year or two in a PHC to “serve the nation.” But when these doctors arrived at their assigned PHCs, they found buildings with no medicines, no equipment, no support staff, and no functioning systems. They were expected to treat patients with nothing.

Some tried. Most realised quickly that the public system was designed to fail.

The moment their mandatory service was complete, they left. They went to cities and started private practices. They joined corporate hospitals. They went abroad. The public system became, in effect, a taxpayer-subsidised training program for private healthcare. The government paid to educate the doctors, then watched them leave because the system it built was impossible to work in.

The doctors who stayed in the public system were either exceptionally dedicated or had no other options. The result was a bifurcation: competent doctors left for private practice where they could actually practice medicine and earn a living, while the public system retained a hollowed-out workforce operating in hollowed-out buildings.

For patients, the message was clear: if you wanted competent healthcare, you paid for it privately. The public system was what you endured when you had no other choice.

Who Steps in When the Government Steps Back?

Then came 1991 and liberalisation.

The economy opened up. GDP growth accelerated, 6-8% annually through much of the 1990s and 2000s. The middle class expanded dramatically. By 2000, roughly 50 million households had crossed into middle-class income levels. By 2010, that number had doubled. Disposable incomes were rising. People had money to spend on healthcare.

And the government was still spending 1% of GDP on empty PHCs.

The state, which had promised to provide healthcare, effectively vacated the field. Not through explicit policy, but through sustained neglect. The public system continued to exist in theory - the PHCs and district hospitals remained on maps, budgets were allocated (and often unspent or siphoned off through corruption), but in practice, the government had stopped trying to deliver healthcare at scale.

This created a vacuum.

And if there is one thing capital hates, it is a vacuum where people are willing to pay money to not die.

Private capital rushed in.

Between 1990 and 2010, private capital poured into Indian healthcare with the kind of enthusiasm usually reserved for gold rushes. Private hospital beds grew rapidly during this liberalisation era. In the last five years alone, $15 billion flowed into the sector. If you plotted healthcare investment on a graph, it would look like a hockey stick.

But here’s what’s strange: despite all that capital, despite all those new beds, supply remains structurally constrained. India still has only 1.3 hospital beds per 1,000 people, less than half of what the WHO recommends and a fifth of what China has built.

So, where did the money go?

The answer reveals something fundamental about how capital behaves when it’s rational.

If you give private equity a choice between:

Option A: Building a network of primary care clinics in tier-2 cities that prevent diabetes through patient education and routine monitoring, or

Option B: Building a 500-bed specialty hospital in Bangalore that does robotic cardiac surgery and orthopaedic procedures for patients with high-limit insurance...

...they will choose Option B every single time.

And for excellent reasons.

Option A generates thin margins (8-12%), requires constant patient acquisition, depends on high volume to break even, and pays back capital over 7-10 years.

Option B generates 25% EBITDA margins, has predictable utilisation from a wealthy patient base, attracts doctors who want to work with cutting-edge equipment, and pays back capital in 4-5 years.

The math is brutally clear. Between 2015 and 2020, India added roughly 50,000 private hospital beds. The vast majority went into tertiary care facilities in major metros - Delhi, Mumbai, Bangalore, Hyderabad, Pune. You can now get robotic prostatectomy, complex cardiac ablation, or advanced oncological treatment performed by surgeons trained at Johns Hopkins, Mayo Clinic, or leading European institutions.

But if you live in Indore or Bhubaneswar and need basic diabetes management, maternal health monitoring, or routine preventive care? Your options remain limited. The neighbourhood clinic with a qualified GP doing systematic chronic disease management barely exists outside the top-tier cities.

The infrastructure that was built reflects capital allocation logic, not population health needs. We first built world-class repair shops for the British gentry in colonial India. Then we built patchwork primary health centres for the many. And now we have a healthcare system optimised for the fortunate urban few in the post-liberalisation era.

The care infrastructure for everyone else remains fragmented across thousands of independent private clinics with wildly varying quality, no systematic protocols, and no coordination.

This wasn’t malice. It was capital doing exactly what capital is supposed to do: flowing to the highest risk-adjusted returns. The tragedy is that the highest-return projects don’t align with what a billion people actually need.

[III] When Beds Do The Eating 🍽️

There is a theory in technology investing that says value inevitably migrates to the “aggregator.” Ben Thompson of Stratechery, who has written more clearly about platform economics than almost anyone, describes how the internet fundamentally changed competition:

“No longer do distributors compete based upon exclusive supplier relationships, with consumers/users an afterthought. Instead, suppliers can be commoditized leaving consumers/users as a first order priority... The most important factor determining success is the user experience: the best distributors/aggregators/market-makers win by providing the best experience, which earns them the most consumers/users, which attracts the most suppliers, which enhances the user experience in a virtuous cycle.”

In this view, software eats the world by controlling the users and commoditising the underlying assets. If you control the travellers, you control the hotels. If you control the searchers, you control the websites.

It turns out that when there are 1.4 billion people and very few hospital beds, the beds do the eating.

Indian healthcare has spent the last five years as a brutal, multi-billion-dollar lesson in supply-side economics. You cannot “aggregate” demand for an ICU bed when there are only 1.3 beds for every 1,000 people. You cannot commoditise scarcity. In a market where people are desperate to not die, the person with the physical room and the oxygen tank is the one with the pricing power.

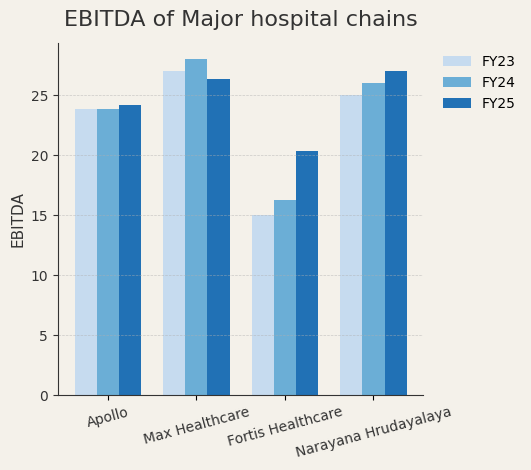

The public markets have priced this reality with a level of enthusiasm usually reserved for companies that sell pixels and have zero marginal costs. India’s top hospital chains trade at 30-50x EBITDA.

I mean, it’s a hospital. It is a building full of very expensive machines and people in scrubs who require salaries. It has all the marginal costs. But if you have the only quality bed in town, the market treats you like a SaaS monopoly.

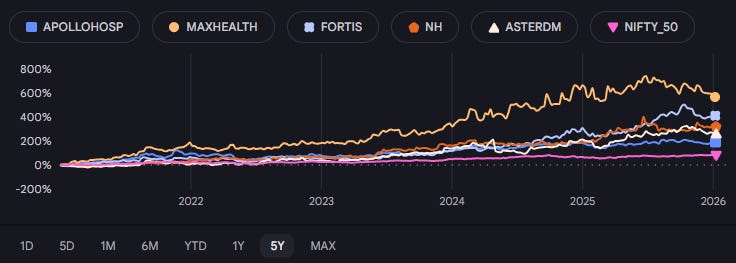

Consider the performance of India’s top five hospital chains - Apollo, Max, Fortis, Narayana, and Aster DM. Over the last five years, this cohort has delivered a 36% CAGR, returning 2.5x the broader Nifty 50 index (~15% CAGR).

This supply rigidity is currently colliding with a massive demand shock. India is famously young. It has a “dEmOGraPhiC DivIDeNd”. It is a country full of twenty-somethings currently powering the global economy, which is a wonderful thing for GDP. But from a healthcare perspective, a demographic dividend is really just a demographic loan that eventually comes due.

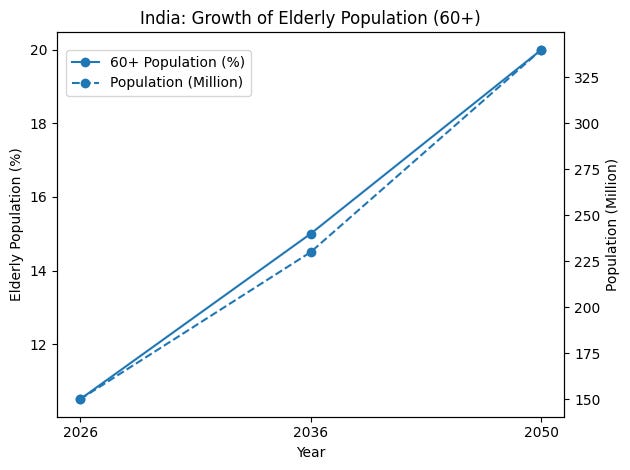

India is aging rapidly in the background. While the world looks at the youth, the 60+ cohort, the people who actually consume the bulk of healthcare resources, is quietly on track to hit 195 million by 2030.

At the same time, the disease profile is shifting in a way that makes the math very attractive for whoever owns the beds. Acute care, ie. getting hit by a bus or catching a one-off infection, is a “bug” in the system. It is episodic and unpredictable. Chronic care for conditions like diabetes or hypertension is a “feature.” It is highly predictable recurring revenue.

If you have 90 million diabetics and 300 million hypertensives, you aren’t running a repair shop for accidents anymore. What you are is something akin to a medical subscription service for an aging population. And in a market with no supply, that is a very good service to be in.

So, Surely There Was A Hospital Boom?

Now, in a normal market, if you saw a business trading at 50x EBITDA, you would expect a massive construction boom. You would see cranes everywhere building new hospitals.

That is not what is happening. Instead, the industry is consolidating. The incumbents are using their capital for M&A, buying up regional players to acquire immediate EBITDA because building a new hospital from scratch involves “regulatory friction” and “gestation risk,” which are professional terms for “it’s a giant headache and takes forever.” Therefore, the preferred playbook remains financial aggregation as opposed to capacity creation.

The approval process requires navigating land acquisition, environmental clearances, fire safety certifications, medical council registrations, and a byzantine web of permissions from multiple government departments that may or may not be incentivised to move quickly. Then you spend 18-24 months on construction, another 6-12 months on equipment installation and staff hiring, and 12-18 months ramping to sustainable occupancy levels.

That’s 3-4 years before you see positive cash flow, during which your capital is tied up earning nothing while accruing interest.

Or you could acquire an existing hospital that’s operating at 60% occupancy, optimise it to 75%, and add ₹50 crores to EBITDA within 12 months without pouring a single bag of cement.

The preferred playbook became financial aggregation rather than capacity creation. Buy existing beds, not build new ones. Roll up regional chains. Extract operational improvements. Show EBITDA growth to justify the 40x multiple.

The result: massive capital deployment, extraordinary valuations, and supply that remains stubbornly constrained.

[IV]The Insurance Inflection

While private capital was building tertiary hospitals and consolidating through M&A, something else was quietly shifting in the background: how Indians thought about paying for healthcare.

For decades after independence, health insurance barely existed. Families were the insurance system. When someone got sick, relatives pooled money. The middle class saved aggressively precisely because there was no other backstop. If a medical emergency hit, you liquidated assets, borrowed from extended family, sold ancestral land if necessary, and hoped the crisis didn’t wipe out three generations of accumulated wealth.

For most people, this was the only option. Until it wasn’t.

Everything Ends Up Being Insurance

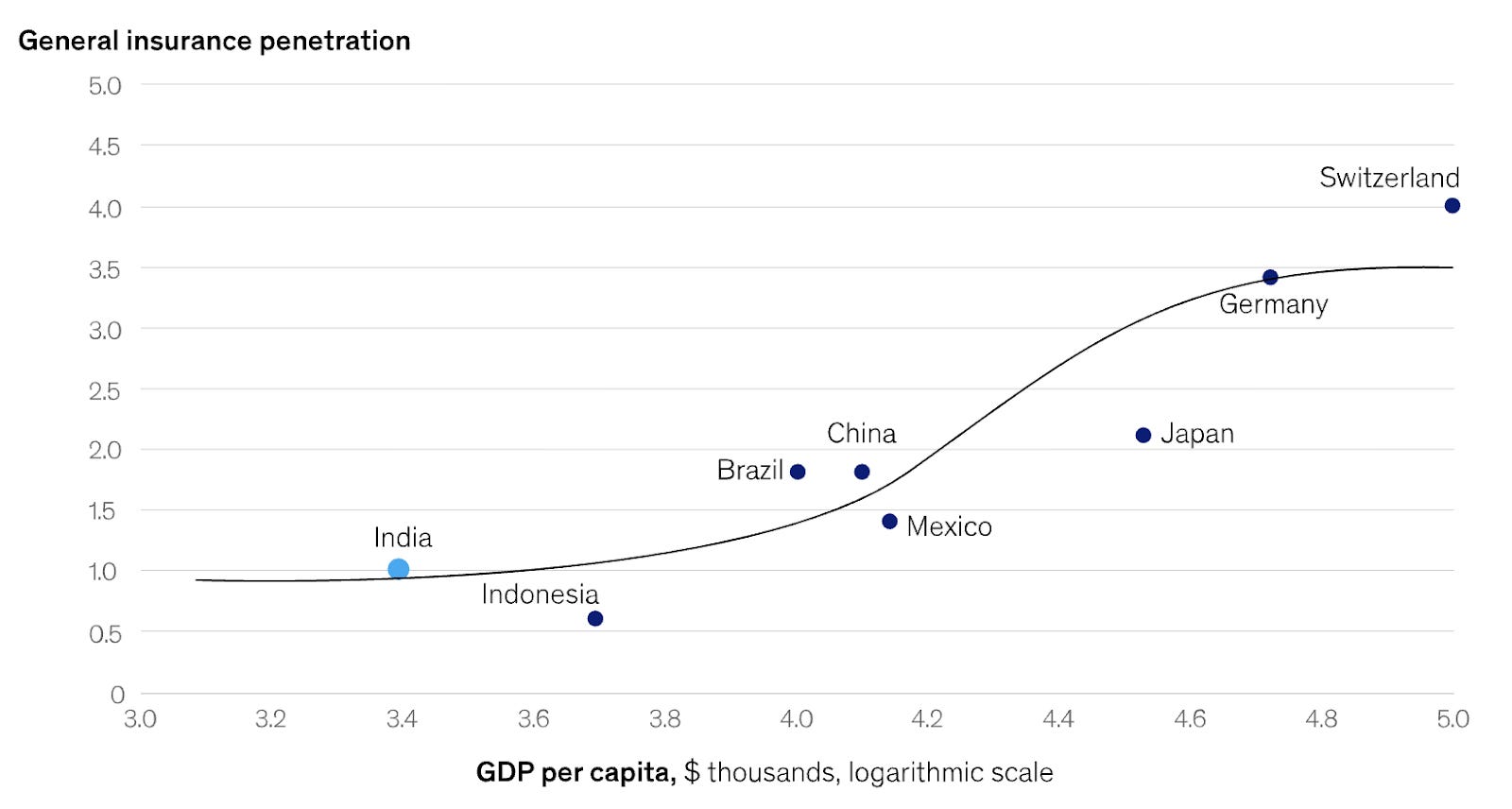

Across every economy that has industrialised over the past century, healthcare follows an identical trajectory: all healthcare spend eventually ends up becoming insurance spend.

A plummeting line showing that as countries get richer, “reaching into your wallet at the morgue” is replaced by “paying a premium to an actuary.”

This is the “Everything Ends Up Being Insurance” hypothesis.

Insurance adoption follows the S-Curve, and it describes the exact moment when a society stops asking their relatives for money and starts buying insurance.

Below $5,000 GDP per capita, insurance is a luxury. You spend your money on things like “food” and “not having the roof leak.” If a medical emergency happens, you self-insure through a combination of your savings account and the generosity of your cousins. Above $35,000, insurance is just part of the background noise of being an adult.

The interesting part is the middle. There is a narrow band, roughly between $5,000 and $7,000 per capita, where adoption really takes off. It’s the inflection point where a population decides that paying a monthly premium is a better deal than having a heart attack wipe out a generation of family wealth.

As per the latest figures from the IMF, India sits at approximately $3,000 per capita today, closer to $13,000 when adjusted for purchasing power. Right at the bottom of that steep part of the curve where things accelerate.

If you look at the numbers, the explosion has already started. Health insurance premiums grew from $6.3B in 2019 to $15B in 2024, a 16.8% CAGR over the last five years.

Now before diving into insurance economics, it’s worth noting that the formula for health insurance companies to make money is fairly simple.

Profit = Premiums - (Premiums * Medical Loss Ratio) - (Premium * Admin Ratio)

And just so we’re all on the same page, we’ll do a quick primer on Insurance Economics for a few paragraphs before moving ahead -

In the insurance business, there is a number called the Medical Loss Ratio (MLR), or, if you are being slightly more neutral, the claims ratio. It is a delightfully cynical name. It represents the percentage of premiums that the insurance company actually has to spend on, you know, medical care.

In any other industry, providing the service you sold is called “the product,” but in insurance, it is a “loss.” If you buy a policy and then have the audacity to actually get sick, you are a liability on a spreadsheet.

Then there is the Admin Ratio. This is the cost of everything else: the rent for the glass office tower, the marketing budget for the billboards, and the salaries of the people whose job it is to figure out if your claim can be legally ignored.

If you add these two together, you get the Combined Ratio.

If the ratio is 95%, the insurance company keeps five cents of every dollar. This is a good day at the office.

If the ratio is 105%, the company is literally losing five cents on every dollar of insurance it sells.

On paper, a company with a 105% combined ratio looks like a very expensive, very poorly managed charity. And yet, some of the largest insurers in the world have run these numbers for decades without going bankrupt. They do this by realising that they aren’t actually in the insurance business; they are in the Float Business.

Float is the Warren Buffett special. It is the money sitting in the insurer’s bank account between the time you pay your premium and the time they actually have to pay for your surgery. If an insurer collects ₹100 from you today and expects to pay out ₹105 in five years, they have effectively just taken an interest-free loan from you. Actually, it’s even better than interest-free; if they invest that ₹100 and earn a 7% yield, they make ₹7 in investment income working off your dime.

The math looks like this:

Underwriting Profit/Loss: -₹5

Investment Income: +₹7

Net Profit: +₹2

At that point, you aren’t really an insurance company anymore; you are a hedge fund that uses future claims obligations as a source of interest-free leverage. Warren Buffett calls this a “negative cost of capital,” and it is the best kind of leverage in the world because, unlike a bank loan, you don’t have to pay it back until someone gets sick.

This strategy works beautifully in life insurance or reinsurance, where you can sit on the money for decades (“long-tail” liabilities). It fails spectacularly in health insurance, where the “tail” is short. People get sick fast. You don’t have twenty years to invest a premium meant for a medical event. You have maybe two months.

In India, the “Float Game” is less of a strategy and more of a distant dream, mostly because the bucket is currently empty: retail health insurance penetration stands at just 0.11% of GDP, and total health insurance at a mere 0.3% of GDP.

You can’t run a multi-billion-dollar hedge fund on interest-free leverage if nobody is giving you the leverage in the first place. As we noted, only about 40% of Indians have a personal health insurance policy. When 60% of your population lacks any coverage whatsoever, your “float” is a series of small puddles that evaporate before you can find a broker.

Back to (the Insurance) Business

Because India is sitting right at the bottom of that vertical S-curve, where nominal GDP is $3,000 and 48% of healthcare is still paid for by people reaching into their pockets at the pharmacy, the industry hasn’t reached the level of “financialisation” where you can ignore the underwriting. In a mature market, you can afford to be a slightly incompetent insurer if you are a brilliant asset manager. In India, you have to be a brilliant insurer because the tail is too short and the pool is too small.

The result is that Indian health insurers are stuck in the most difficult version of the game. They don’t have the “long-tail” luxury of life insurance to build a Buffett-style empire, and they don’t have the mass-market penetration to make up for thin margins with sheer volume. They are trapped in a world where they have to make money the hard way: by actually making sure their “Medical Loss” doesn’t swallow the whole rupee.

And since they don’t control the hospital, and they don’t control the doctor, and the “Float” isn’t there to save them, they do the only thing a rational, trapped financial entity can do. They build the trapdoors. They write the fine print. They hire people to say “no.”

They realise that since they can’t be a hedge fund, they have to be a fortress. They protect their 2% EBITDA margin by making sure you never get to see it. It is a perfectly logical response to a structurally impossible position.

In fact, if you look closely at the entire ecosystem, you’ll find that everyone is behaving with the same level of cold, mathematical logic. The system isn’t failing due to bad actors, but because rational participants have done the math and concluded that the current equilibrium is the only way to remain solvent. To fix it, you have to understand that the ensuing madness is actually a form of sanity.

[V] Why Is Everyone Acting Rationally?

The madness starts with a very simple instrument called Fee-for-Service (FFS). It is exactly what it sounds like: you show up, the doctor does a thing to you, and you (or your insurer) pay for that thing. If the doctor does two things, you pay for two things. If the doctor does ten things, like ordering an MRI for a tension headache, you pay for ten things.

In any other industry, this is just how a store works. If you go to a hardware store and buy ten lightbulbs, you pay for ten lightbulbs. The problem is that in healthcare, you don’t actually know if you need ten lightbulbs. You are relying on the guy who sells lightbulbs to tell you how dark it is.

The incentive here is not complicated: if you get paid per “thing,” you have a very strong financial reason to find more “things” to do. This would be fine if more things were correlated with you not dying, but in medicine, the correlation between “total billing” and “clinical health” is essentially a random walk.

This creates a brutal principal-agent problem. You, the patient, are the principal. You want to get better. The doctor is your agent. The doctor is supposed to act in your best interest. But the doctor’s paycheck comes from doing procedures, not from keeping you healthy, so their incentives don’t always align with yours.

Most doctors in India’s private hospital system aren’t actually salaried. They operate under something called a “Minimum Guarantee “(MG), a contract structure where the doctor receives a fixed payment only if they generate a predetermined revenue target for the hospital. If they don’t hit the target, they earn less. If they exceed it, they keep a percentage of the overage.

This is perversely expressed in metrics like “OP/IP conversion ratio”, the rate at which a doctor converts outpatient consultations into inpatient admissions. The doctor is literally judged on how many patients they can convince to get admitted.

Similarly, an orthopedic surgeon, for instance, might receive 30-40% of the revenue from every surgery they perform. Let’s model the choice architecture. A patient presents with knee pain.

Option A: Prescribe physical therapy. Revenue: ₹20,000. Surgeon’s Commission: ₹0.

Option B: Recommend a knee replacement. Revenue: ₹5 lakh. Surgeon’s Commission: ₹1.5-2 lakh.

This is a perfectly designed principal-agent structure. The patient (the principal) wants the best medical advice and medical outcome at the lowest possible cost. The agent (the doctor) wants a good medical outcome at the highest reasonable cost they can conscience.

The economists call this “supplier-induced demand.” You might call it a nightmare.

In theory, this aligns payment with work done. In practice, it creates an incentive structure of almost breathtaking perversity. The system’s KPI is not “patient wellness” or “positive health outcomes.” It is “activity.” The business thrives not on health, but on sickness, and specifically, on the treatment of sickness:

More tests? More revenue.

More procedures? More revenue.

Longer stays? More revenue.

That surgery you might not need? Definitely more revenue.

You might say, “But doctors have ethics!” And they do. But they also have compensation plans.

The doctor isn’t evil. The doctor is just trapped in a system where “doing more” is financially rewarded and “doing less” looks like underperformance. If the hospital spent ₹80 crore on a CT scanner and it’s sitting idle, someone in the finance department is asking why. The doctor, consciously or not, becomes the solution to that problem.

And that’s before we even get to the Estimate Desk.

Many hospitals operate an “estimate desk,” which is a polite term for a bespoke price discovery unit that operates at the point of maximum emotional leverage. When a patient arrives, typically in an emergency with zero bargaining power, the desk provides an “estimate.”

This estimate is not a function of the medical procedure alone. It is dynamically priced based on real-time data signals of the customer’s ability to pay.

Wearing a Rolex? Estimate ↑

Arrived in a Mercedes? Estimate ↑

Mentioned insurance? Estimate ↑↑ (hospital knows insurer will negotiate, so start high)

Address in a wealthy neighbourhood? Estimate ↑

This is textbook price discrimination, the kind of yield management airlines use for seats. Except the variable isn’t your travel flexibility; it’s your desperation to see a loved one survive.

In India, to run anything other than a “pay-per-procedure” model, you need a pool of insured lives large enough to make the actuarial tables look like a plan rather than a random number generator. If only 40% of your patients have insurance, you aren’t “managing the long-term health of a population.” You are just running a retail shop where people show up when they are already broken.

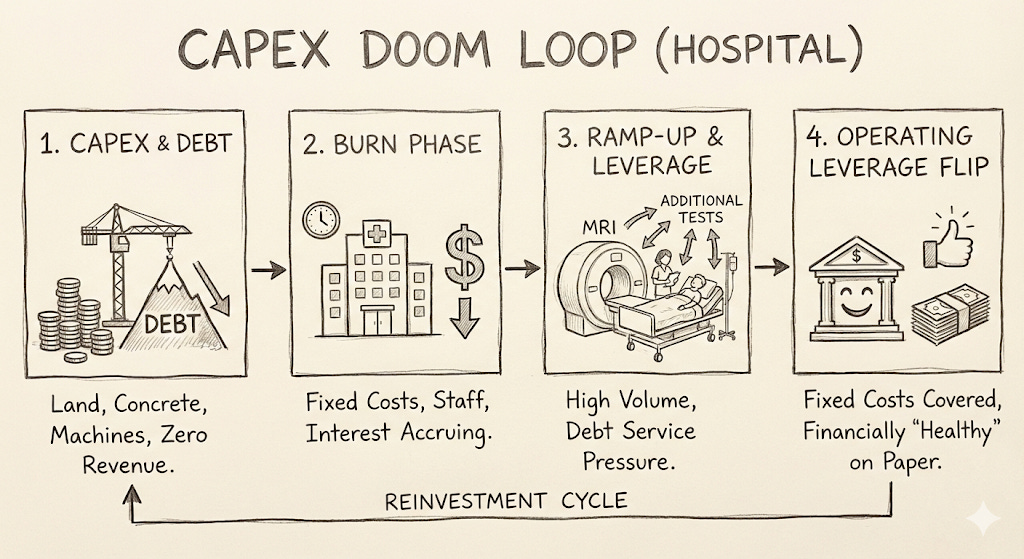

In a market where 60% of customers are paying cash, the hospital has no incentive to keep you healthy and every incentive to make sure you pay your bill before you leave. But even if everyone had insurance, you’d still run into the Capex Doom Loop.

The financial life of a hospital begins with a very long period of spending money you don’t have on things that don’t yet work. You spend years pouring capital into land and concrete and machines that cost more than small islands.

During this phase, you have zero revenue, but you have a mountain of debt that is accruing interest with terrifying discipline. Debt, unlike patients, never misses an appointment.

By the time you actually open the doors, you are already in a deep financial hole. You have to hire a full staff of surgeons and nurses and keep the lights on in the ICU, regardless of whether there is anyone actually in the beds. This is the “burn” phase, where the hospital is a building of fixed costs and the only thing being utilised is the bank’s patience. Your lenders begin asking very reasonable, very pointed questions about when exactly this project is going to stop being a theoretical exercise in architecture and start being a business.

This is where the math of “operating leverage” becomes the hospital’s best friend and the patient’s most expensive problem. In the ramp-up years, the hospital is still gasping under the weight of its debt service. Every additional MRI, every extra night in the ICU, and every “thorough” metabolic panel is a contribution to the interest payment.

Eventually, if you get enough people through the door, the leverage flips. The fixed costs are covered, the bank is happy, and the hospital finally looks financially healthy on paper. It’s just that getting “healthy” on paper usually involves a lot of people getting a lot of tests they probably didn’t need.

This where the doctor’s principal-agent problem and the hospital’s debt repayment schedule fuse into a single economic machine. The hospital needs volume to service its debt. The doctor needs to hit revenue targets to keep their compensation. The patient needs care. Only one of these three parties has the information asymmetry to make it all work, and it’s not the patient.

If you are a health insurer in India, you are watching this happen from the other end of a very long, very expensive assembly line. In a fragmented network of thousands of hospitals, you are just a check-writer. You can’t stop the doctor from ordering the MRI. You can’t influence the care pathway. You are just standing there, trying to figure out how to pay as little as possible for a process you don’t control.

On paper, your industry is booming. In reality, you are trapped in an inflationary spiral where the growth is coming from the size of the invoices, not the number of customers.

To understand why this is happening, you have to look at the two different buckets of the business: Group and Retail.

Group insurance is what your HR department buys in bulk for 10,000 employees. In 2020, the regulator introduced a mandate requiring all employers to provide group health coverage. This was “forced adoption” for 150 million formal-sector workers. It was supposed to be the moment the industry finally achieved the scale needed to make the math work.

Instead, it acted as a massive dinner bell for the cathedrals of healthcare: the hospitals.

When you inject 150 million people into a healthcare system with “company money” in their pockets, hospitals react the way anyone with a mortgage and a monopoly reacts: they stop worrying about price. In the old world, where patients paid out-of-pocket, hospitals had to be somewhat sensitive to what a middle-class family could afford. In the new world, the “Payer” is a faceless corporation. Price sensitivity evaporated, and hospitals began raising procedure costs to service their massive debt.

The doctor, meanwhile, stopped being the gatekeeper of medical necessity and became the facilitator of billing. When the patient isn’t paying, the doctor doesn’t have to justify the third blood test or the “precautionary” specialist consultation. The insurance company is paying, the hospital’s revenue per patient is climbing, and the doctor’s commission is looking very healthy. Everyone wins, except the system itself.

On the other hand, retail insurance is what you buy for your family at the kitchen table because you’ve realised that life is fragile and your savings account is thin. Because insurers don’t control the hospitals, they have to pass those rising “Group-driven” costs back to the only people they can: the policyholders.

The numbers tell the story of this hollowing out. Over the last decade, total premiums in the retail market have grown 5x, but the number of lives covered has only grown 2.5x. If your revenue is up 500% but your customer base is only up 250%, you haven’t “democratised” the product, you have just made it exponentially more expensive for the people who already had it.

This triggers a classic Adverse Selection Death Spiral. As premiums rise to cover medical inflation, the healthy retail customers, the ones who don’t expect to get sick, decide the price is too high and drop their policies. This leaves behind a pool that is sicker, older, and more expensive. That, in turn, justifies the next premium hike, which pushes out the next layer of healthy people.

The result is a system that isn’t expanding as much as it is getting heavier. The “premium per life” is going parabolic because the industry has moved from a “growth business” to a “cost-recovery business.” Standalone insurers are now price-takers in a market where they have no control over the actual product (healthcare).

Since they can’t control the cost of care, they have pivoted to a new business called friction engineering.

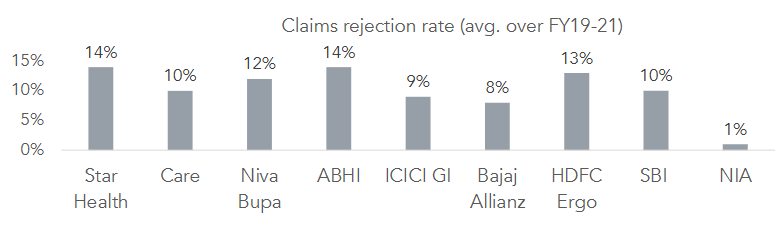

India’s leading insurers have managed to keep their claims ratios at 60-65%, but they haven’t done it by making healthcare cheaper but by making it harder to get. Claims rejection rates now average 10-14%.

This creates a high-churn, high-unhappiness trap where the rational choice is wanting to switch their insurer. But they can’t switch, because if they’re sick, the next insurer will exclude their “pre-existing condition”. You are trapped in a relationship with a company that makes money by saying “no” to you.

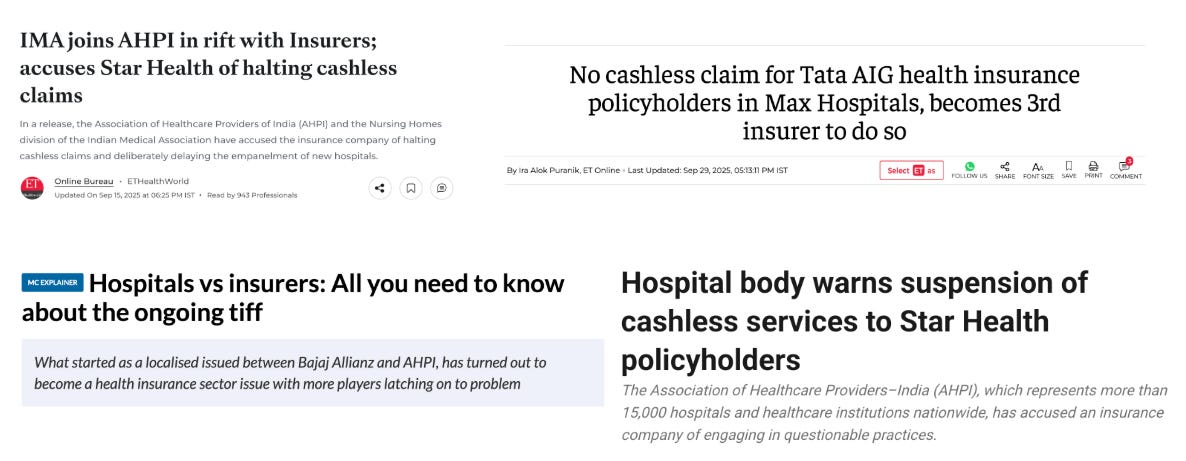

This tension eventually turned into an actual war. In September 2025, the major insurers (Star Health, Tata AIG) ended “cashless settlement” at Max Hospitals, one of India’s elite chains. The insurers accused the hospital of overbilling and naturally, the hospital accused the insurers of underpaying.

The patients, who had paid their premiums precisely so they wouldn’t have to worry about this, were told they had to pay out of pocket and “file for reimbursement later.” This is what happens when the “friction engineering” of insurance hits the “physical reality” of a hospital’s debt schedule and a doctor who is measured on how many patients they admitted today.

The fundamental problem is that no one controls utilisation. The doctor is supposed to, but the doctor is paid to do more. The hospital wants the doctor to do more. The insurer wants the doctor to do less, but the insurer doesn’t employ the doctor. Ultimately, the standalone insurer is a price-taker. When a hospital chain hikes procedure prices by 12%, the insurer has two choices: absorb it (hurting margins) or reject it (hurting customers).

Currently, they are choosing to hurt customers.

If you zoom out far enough, what the Indian healthcare system has built is a remarkably efficient luck-sorting machine. If you are lucky enough to live in a major city, lucky enough to have insurance that actually pays, lucky enough to work for a company with good group coverage, lucky enough to have an acquaintance who knows how to navigate a hospital - you get reasonable care. If you are unlucky in any of these dimensions, you get the other version.

The system isn’t cruel. It’s indifferent. And indifference, at scale, is its own kind of cruelty.

Someone had to decide that was unacceptable. Someone who had learned, young, what luck actually meant in a hospital.

[VI] The Company

How do you remove luck from the business of staying alive?

How do you remove luck from the business of staying alive?

If you are seventeen years old and watching your uncle die of pancreatic cancer, you might expect to learn something about biology or the limits of modern medicine. But if your father is a consultant for the NHS who can navigate the bureaucracy, coordinate the specialists, and pay for the procedures, you mostly learn something about circumstance.

Mayank Banerjee’s bauji, his paternal uncle, the person he was among the closest to in his extended family, was diagnosed with pancreatic cancer when Mayank was thirteen. He died four years later. It was the only time in his life Mayank cried. But what stayed with him wasn’t just the grief. It was the unfairness of it all.

His father, an ENT consultant who had moved the family from Agra to the UK for an NHS posting, could do things that a normal Indian family couldn’t. He knew which specialists to call. He knew how to read a treatment plan and push back on it. He could absorb costs that would have bankrupted most. The uncle got four more years partly because of medicine and partly because of who his brother happened to be. Without that accident of family, the outcome would have been different. The care would have been different. The timeline would have been shorter.

“The world is unfair and based a lot on luck,” Mayank says. “How do we remove the element of luck when it comes to the welfare of the people we love?”

This is the question Even is actually trying to answer. Everything else — the insurance structures, the hospital economics, the capitation contracts — is downstream of this.

How to Save Democracy (And Why Nobody Wanted You To)

Mayank followed the standard trajectory for people who are destined to either solve global problems or become deeply frustrated trying. He went to Oxford on a PPE degree, became president of The Student Union - a platform famous for producing a disproportionate number of British prime ministers - and found himself in rooms with people who ran things.

What he eventually realised was that the policymakers of the world were trying to keep old, creaky systems from falling over. The entrepreneurs and tech founders, on the other hand, were building new ones. While at the Union, he met founders like Eric Schmidt and Jack Dorsey, and found them more impressive than anyone in government or policy. What hammered home his epiphany was realising that, a century ago, someone with his credentials would have been expected to go out and run a country. Now, they become investment bankers and consultants. Mayank decided to drop out and started a company instead.

His first company, built with Matilde ‘Mati’ Giglio, a close friend he’d met at Oxford, was called Compass News. The premise: young people were making bad political decisions because they were poorly informed. The solution: machine learning that curated better news feeds. The logic was airtight. The only flaw was that young people, it turned out, did not particularly want to be better informed.

It was, as Mayank would later describe it, a vitamin masquerading as a painkiller. Nobody was sick enough to take it.

They decided to move on to other pursuits. Mati moved into venture capital. Mayank, restless and back to square one, returned to India looking for ways to be useful.

Fixing The Bill

The real moment of conception for Even is hard to pinpoint because there wasn’t a single eureka moment. There was a decade of accumulating dots — a close uncle passing away, a rejected YC application, a pandemic, a cold email to a then-stranger in Mumbai — that eventually cohered into something concrete.

When Mayank moved back to India on New Year’s Eve 2018, he brought a list of problems he wanted to examine further. If you are a normal person and you see a country with “massive structural problems,” you might think about moving to a nice, quiet suburb in Switzerland instead. But if you are an entrepreneur, that massive structural problem becomes an invitation.

The logic here is a form of the ‘Venture Capitalist’s Prayer’: scale compounds solutions the same way it compounds problems. If you can find a way to fix something for one person in India, you have a statistical head start on fixing it for a billion more.

Two problems on Mayank’s list kept bubbling to the top. The first was healthcare: the fact that 55 million Indians are pushed below the poverty line every year because they had the audacity to get sick. The second was whether India’s “demographic dividend” — the polite way of saying “a terrifyingly large number of young people who need to be productive” — would actually pay out, or if it would just be a demographic liability. He could not quite figure out a sustainable solution for the latter.

So he started with healthcare. And he called Mati.